Fintech summer continues as insurtech giant Accelerant, long-rumored for IPO, debuted on the New York Stock Exchange under the ticker ARX. The company is an AI-enabled insurance marketplace that matches risk capital providers with underwriters.

Shares initially priced at $21 and opened more than 30% higher; the IPO is expected to raise more than $720 million. Prior to the company’s decision to go public, Fintech Nexus had a chance to catch up with CEO and cofounder Jeff Radke about his vision for the firm, and understand how AI is changing the way insurance works. (We also simplify the complex network of sidecars, reinsurers, platforms, and specialty insurers that make up the Accelerant ecosystem.) That interview is below.

In other news: Move over details, in the age of AI, the devil is in the data. Last week’s JPMorgan announcement on customer data ownership sent the fintech world into a major upheaval and poured cold water on the momentum around the future of open banking, with advocates pushing back hard. A spokesperson for the Financial Technology Association told Forbes that Chase’s new cost structure is designed “to crush competition, levy a tax on fintech innovation, and cement their power in the marketplace.” Fighting words.

The battle continues as today SOLO — a sharing network designed to ensure that verified customer data is portable, protected, and equitably governed across institutions — emerged from stealth to challenge the “legacy bureaus and aggregators” with a Customer Data Clearinghouse, which compensates the go-betweens for their data (read: pay the banks doing the operational work).

How long will the music last at SOLO’s industrial cotillion? It may partially depend on the future of open banking, which the FTA is fighting for in the courts (as we’ve covered). In the meantime, SOLO is framing its revenue model as a reflection of the costs involved in trust enablement, rather than data ownership tout court. “Banks are stepping up to say, ‘We incur the costs. Why should third parties set the price?'” SOLO founder Georgina Merhom told Axios.

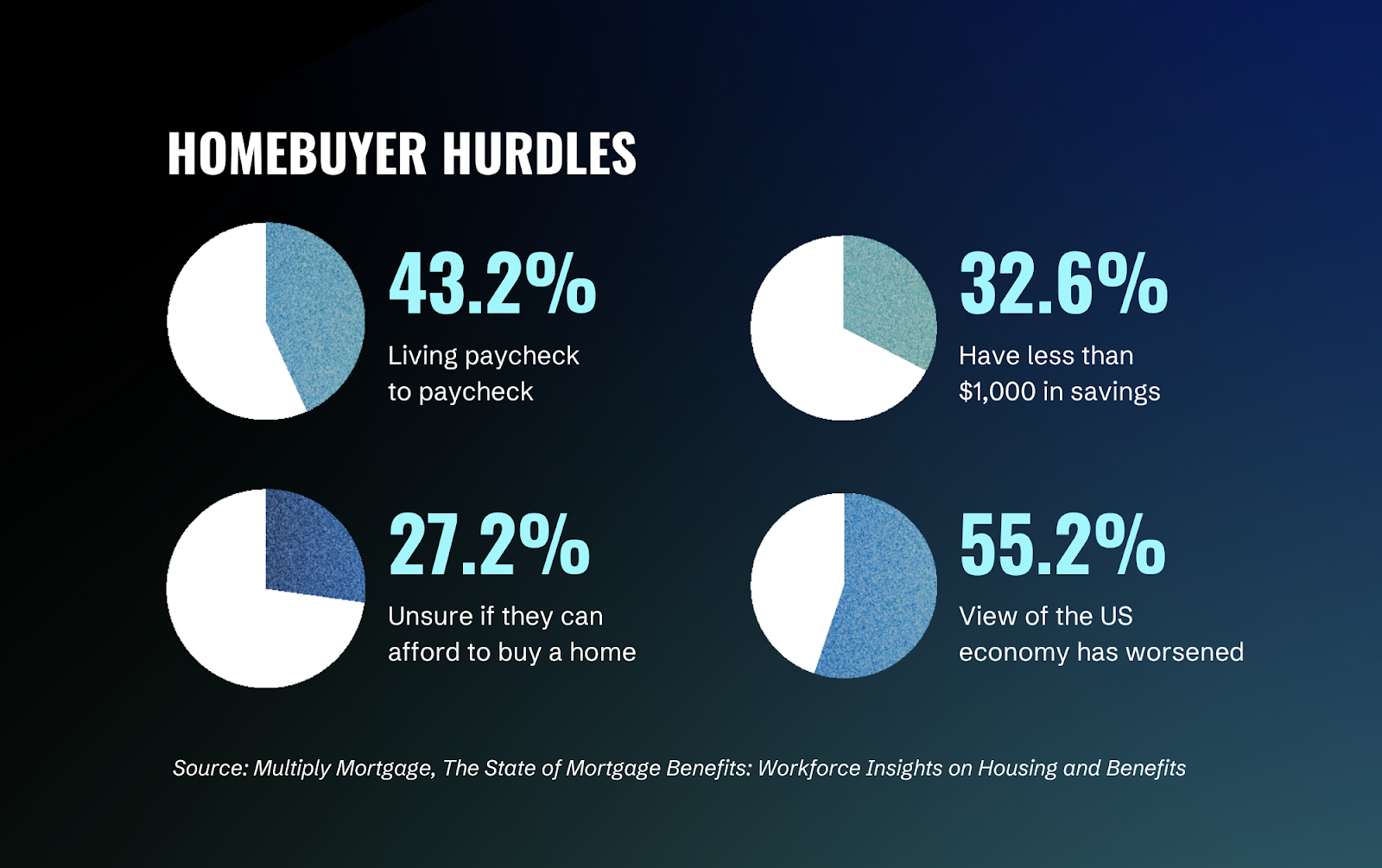

And it’s back to the future in the housing market: Home sellers now outnumber buyers by half a million per Redfin, but no one is cutting prices, and the rates are vintage 1980s at just under 7% for a 30-year fixed. What’s a prospective new homebuyer to do? Apparently ask their employers to help them pay for it (beyond a typical paycheck).

Employee mortgage benefits and programs helping employees access or manage home financing have been gaining traction — often through discounts, partnerships, financial education, and/or direct financial support. In a new survey from Multiply Mortgage, three-quarters of respondents said they would be “more likely” to join a company that offered support getting a lower mortgage rate, and a majority said access to a lower rate through an employer would be “extremely valuable.”

“People are under financial pressure, and homeownership feels further out of reach than ever. Employers are looking for meaningful ways to help, especially when budgets are tight,” Multiply CEO Michael White said, adding that mortgage benefits may be that silver lining.

–The Editors