It is earnings season and today LendingClub announced their Q4 2017 earnings. Last week we covered OnDeck’s Q4 results as they reached an important milestone of achieving GAAP profitability. As LendingClub CEO Scott Sanborn appropriately stated on the earnings call, 2017 was a year of transformation for the company.

To that end, LendingClub shared that they settled two class action lawsuits, one at the state level and the other at the federal level. These lawsuits stem from the issues in 2016 which led to then CEO Renaud Laplanche exiting the company.

While this is good news for LendingClub to have these lawsuits behind them, there are still other ongoing investigations and the settlements came at a significant cost. The total settlement was $125 million with $47.75 million covered by insurance and the remaining $77.25 million covered by the company. LendingClub had planned for these costs and so they will not have an affect on the operations of the company. Other government investigations ongoing include those from the SEC, FTC and the DOJ. In addition there may be legal costs related to indemnification obligations.

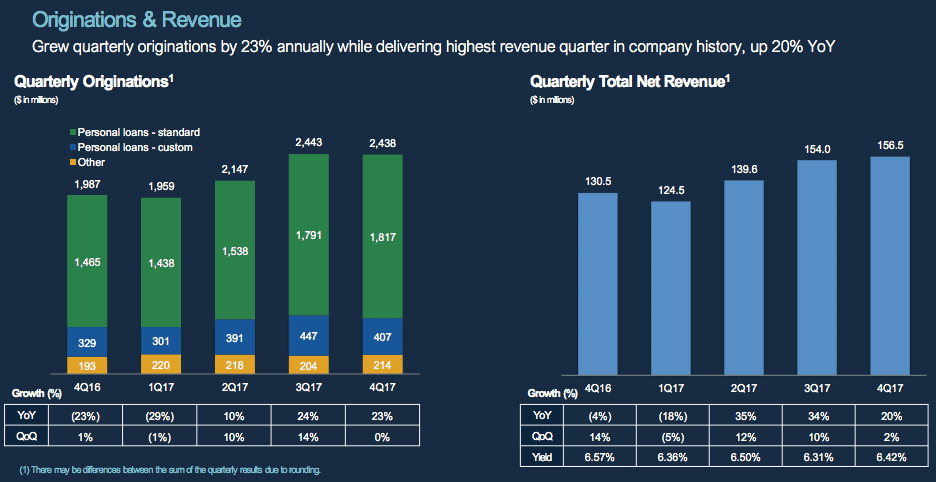

Moving on to the financials for the quarter, LendingClub delivered another record quarter of $156.5 million in revenue up slightly from their previous quarter. Originations were slightly down from the third quarter at $2.436 billion. They reported a GAAP net loss of $92.1 million in the fourth quarter which was affected by the class action litigation settlement expense.

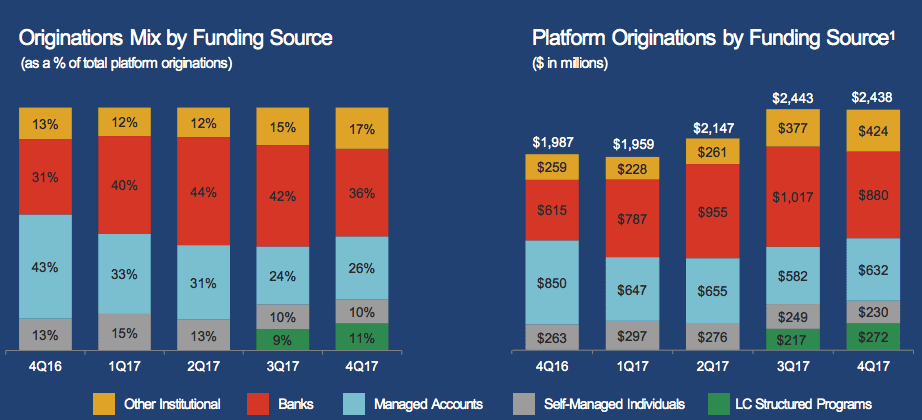

Originations by funding source remained fairly stable for the quarter. Bank participation was down slightly in part due to the previously shared news that LendingClub would be working with Credigy in a different format. LendingClub also highlighted their CLUB Certificates which are part of “LC Structured Programs” below. We covered the announcement of CLUB Certificates in depth back in December 2017.

On the earnings call there was a lot of discussion about efficiency, both on the borrower side as well as internally. One change LendingClub has made was signing a multi-year deal with a loan servicing platform to drive down operating costs. Sanborn noted that the engineering resources that were previously dedicated to maintaining an internally built system will be better allocated to working on projects related to LendingClub’s competitive advantages. Moving to the unnamed industry standard provider will also give the company operational flexibility and allow the company to integrate easier with third parties.

While LendingClub continues to test new marketing channels as well as ways to improve take rates, Sanborn mentioned that the market overall is still under-penetrated. Increasing awareness of smarter solutions such as LendingClub loans will only help the company. In Q4 LendingClub launched a feature which allows consumers to directly pay off existing credit card debt.

Another topic which is on many investors’ minds is interest rates. LendingClub believes they are well positioned in a rising interest rate environment due to the short duration of the product as well as the low cost of capital. As the cost of credit for consumers continues to increase, LendingClub will still be an appealing option to consolidate credit. Sanborn noted that increasing interest rates may serve as a wake up call to consumers and prompt them to look for other solutions. He also shared that the types of investors that participate on the platform will continue to evolve as interest rates rise. The only change related to LendingClub loans was that longer term, high risk loans received modest rate increases.

In the third quarter, LendingClub announced their new credit model. While these loans are still very young, they see positive early signs. Related to performance, one analyst asked about the relative increase of sales and marketing expenses today compared to a time in the past when LendingClub was originating about the same volume of loans. According to Sanborn the biggest driver of the increase were LendingClub’s own actions to contract on credit to drive returns to investors.

LendingClub provided the below guidance for Q1 2018 and reaffirmed their guidance for 2018:

First Quarter 2018

- Total Net Revenue in the range of $145 million to $155 million

- Net Income (Loss) in the range of $(25) million to $(20) million

- Adjusted EBITDA in the range of $5 million to $10 million

- Reconciling Items between net loss and non-GAAP adjusted EBITDA consisting of stock-based compensation of approximately $19 million, and depreciation and amortization and other net adjustments of approximately $11 million

Full Year 2018

- Total Net Revenue in the range of $680 million to $705 million

- Net Income (Loss) in the range of $(53) million to $(38) million

- Adjusted EBITDA in the range of $75 million to $90 million

- Reconciling Items between net loss and non-GAAP adjusted EBITDA consisting of stock-based compensation of approximately $77 million, and depreciation and amortization and other net adjustments of approximately $51 million

Conclusion

There are a couple big themes I see after listening to the earnings call and looking more broadly at the economy: increasing interest rates, and consumer debt reaching all time highs. While I am less sure about what will happen as interest rates rise for these companies, it’s clear there is still a massive opportunity for companies like LendingClub. This is the opportunity that we and many in the marketplace lending industry have been talking about for years. The market still remains under-penetrated as Sanborn pointed out and it isn’t clear what it will take for consumers to truly embrace online loans like those offered by LendingClub. For many years we’ve been in a low interest rate environment and as the expected rate hikes come into play in 2018 it’s going to be interesting to see the effects on both the borrower and investor side.

Disclosure: Peter Renton, the founder and CEO of Lend Academy, and Ryan Lichtenwald, the author of this article both own LC stock.