Last week Bloomberg published a lengthy piece titled “How Lending Club’s Biggest Fanboy Uncovered Shady Loans”. The article focuses on Bryan Sims, an individual investor who, like many people, has taken an interest in Lending Club and was attracted to the transparency of their loan book. He decided to do some detailed analysis on this loan book.

There are two key takeaways in the article. First, it discusses the loans taken out by Renaud Laplanche and his friends and family back in 2009 that was done supposedly to inflate origination numbers which has been widely reported. This was a significant misstep in my opinion, so I have little issue with any of the points made about this.

Second, the article discusses the fact that Lending Club doesn’t report when borrowers take out a second loan. Now, before we go any further I should say that I have been urging Lending Club to disclose this kind of information since I first met with Renaud Laplanche and Scott Sanborn back in 2011. But the fact is the article misconstrues so much here that I felt like a response was needed.

The Missing Pieces Not Mentioned in the Article

Here is the major issue I have with this article. The Bloomberg reporters imply that Lending Club has lax underwriting standards because the same person has taken out two different loans at different rates:

It was one person with two active loans, and Lending Club was treating them as completely unrelated, charging wildly different interest rates. The borrower was paying about 15 percent interest on one loan of about $15,000; on the other, he was paying 9 percent on twice the principal. That meant the investors who held only the second loan were leaving money on the table. And Lending Club didn’t seem to be doing anything to help them.

Let me explain how Lending Club, or any online lender for that matter, works. A borrower takes out a loan and Lending Club analyzes their financial situation at that moment and provides an interest rate (assuming they are approved). If this same borrower takes out a second loan Lending Club analyzes this person’s new financial situation and makes a decision based on that. It is quite possible that a person’s financial situation has changed – the first loan could have been used to pay down higher interest credit card debt for example. This could even be the case for a borrower that was taking out two loans within a month of each other which was another example given in the article.

Now, we should point out that Lending Club has rules on taking out a second loan. Typically, borrowers have to wait 6, 9 or 12 months in order to take out a second loan depending on a number of credit factors. Prior to 2013 there was an exception to this – for borrowers who did not get their loan fully funded. They could re-list the portion of the loan that was not fully funded within this minimum window. But there has not been a loan go unfunded at Lending Club since 2013 so that is a moot point today.

Transparency and Prosper Performance

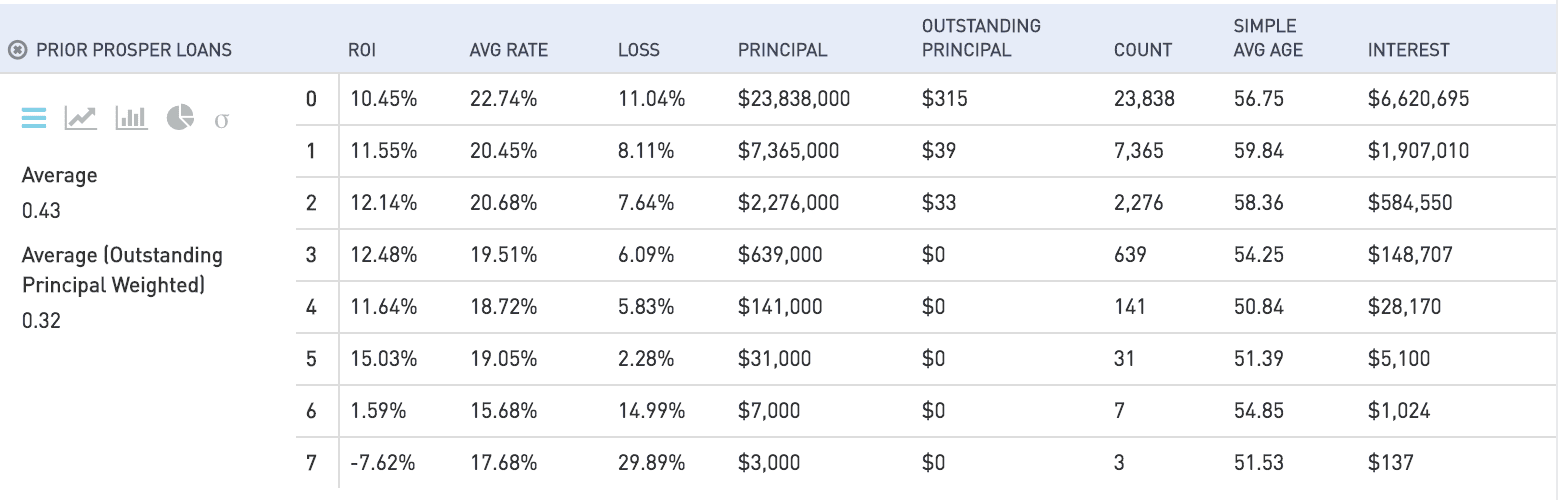

Having said all this, I believe Lending Club should be providing details on repeat borrowers. Why? Because repeat borrowers actually perform BETTER than borrowers who take out just one loan. Allow me to explain with examples from Prosper. Lending Club’s rival provides details on repeat borrowers – in fact Prosper has 15 elements exposed including details on loan amount, earliest pay off, number of prior loans, number of prior loans still active, balances outstanding, details on late loans etc.

Anyone (including Bloomberg reporters) can use NSR Invest to analyze loan performance on any of these filter criteria and through this you can get a really good understanding of how repeat borrowers perform.

Take a look at the graphic below. I filtered on all loans that were originated prior to June 1, 2013 to focus on 36 month loans that were pretty much fully mature. This table provides ROI information on the borrowers based on number of prior Prosper loans. What is interesting is that borrowers with two prior loans perform better than borrowers with one prior loan and they both perform better than new borrowers.

[slb_exclude]

[/slb_exclude]

I first wrote about this phenomenon back in 2011 and to this day I still maintain repeat borrowers as one of my selection criteria when investing in loans on Prosper. This is the main reason I lobbied hard for this inclusion at Lending Club.

Conclusion

Lending Club has many challenges, of that we are all aware. But weak underwriting is not one of them. While it is far from perfect it is so much better than this article implies. Sure there have been minor upticks in defaults from time to time but investor performance has been strong now for many years.

To make assumptions based on incomplete facts is dangerous. Bryan Sims assumed he knew more than Lending Club. More than an experienced credit underwriting team with decades of experience underwriting consumer loans. The Bloomberg reporters agreed with Bryan Sims, that maybe he did know more. A deeper analysis would have led to a more complete story but probably one that would have been less controversial. And in the end the story should have come to a quite different conclusion.