“If you’re feeling confident managing things at home, you can feel confident at work. And if you feel confident at work, you should definitely feel confident bringing that knowledge back home.” – Lindsey Stanberry, founder of The Purse

For many founders and executives, managing money at work feels like second nature. You’re fluent in KPIs, budgets and revenue goals. But at home, those same people often describe their finances with very different language: “trial and error,” “arguments about the credit card” or “I just let my partner handle it.”

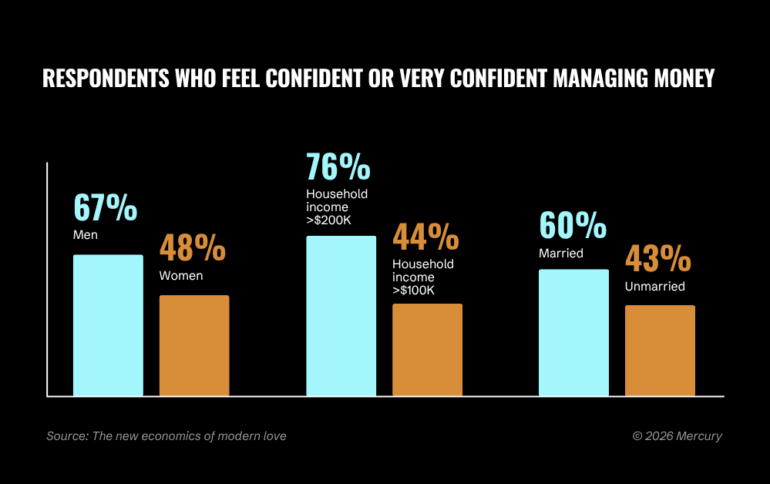

That disconnect is at the heart of new research from Mercury called The New Economics of Modern Love, based on a survey of 1,400 U.S. adults in committed relationships. The data highlights how couples manage money — and what it reveals about the state of financial literacy and financial leadership today.

In a recent conversation about the study, Lindsey Stanberry, founder of The Purse and long-time finance journalist, unpacked what it means to be a kind of dual CFO: one for your career, and one for your household.

Couples Are Confident…but

On the surface, the Mercury study suggests people feel reasonably good about their financial lives.

Confidence around money management showed up as a gap in demographics: More men than women felt confident, the more money you have, the more confident you are and those married versus unmarried were more confident.

Not as much of a surprise, as Stanberry noted that the data challenges the usual narrative of money as a primary source of friction between partners. Confidence around money is not purely about competence. It tracks how you were taught or not taught to think about it from the beginning, she said.

That said, 57% of couples in the Mercury study felt financially confident.

“There is always this feeling that couples have a lot of tension with money, and this tells a different story,” she said. “When couples are working together to manage their finances, they feel more confident, and there’s a lot of trust there.”

A few things did stand out: Men self-identify as the financial leader at nearly twice the rate of women, 38% to 21%. Despite that gap, around 80% of those same couples say their finances feel fair. Perhaps more shocking, nearly half said they learned money management through trial and error.

In other words, couples feel things are “fair,” yet women are less likely to see themselves or be recognized as financial leaders, even when they’re heavily involved.

The CFO at Work vs. the CFO at Home

Stanberry frames much of this through the lens of leadership, particularly women who are effectively acting as CFOs in both their professional and personal lives.

When you look at corporate financial services leadership, the men versus women pattern from the Mercury study repeats. Women hold approximately 19% of C-suite roles in the industry. In the Fortune 500, they hold about 8 to 10% of CEO roles and roughly 17 to 18% of CFO roles. The numbers move slowly and the roles themselves tell a subtler story.

“That study was so slightly depressing because the women in those leadership roles were not often CFOs,” Stanberry said. “They were often more operational roles or marketing roles, less about actual hard data and investment.”

The parallels are hard to miss: women do a tremendous amount of financial work both professionally and personally but are less likely to be framed, or to frame themselves, as the people “in charge” of the money.

At home, the division of labor often falls along traditional, gendered lines, Stanberry said. Women are frequently the “password keepers” and bill payers, while men are more likely to see themselves as strategic decision?makers. For example, women may manage the money in households but their husbands manage accounts.

So “the day-to-day versus the long-term,” she said. Operational versus strategic. Execution versus vision.

However, the skills required to manage a household budget and a career are deeply connected, Stanberry said.

“If you can understand how to run your home: to manage your budget and to manage your money, that leads to confidence in all the things that you do at work,” Stanberry said. “Especially in this day and age when layoffs are so rampant, understanding how you contribute to your company’s bottom line is really important. It’s a two?way street: if you’re feeling confident managing things at home, then you can feel confident at work. And if you feel confident at work, you should definitely feel confident bringing that knowledge back home.”

The State of Financial Literacy

When it comes to the state of financial literacy, there’s more information and content than ever, Stanberry said. She sees high schools teaching personal finance to influencers and AI, but the quality and context are often uneven.

“The internet is filled with financial influencers who offer like a mixed bag of advice,” she said. “Take what your parents say with a grain of salt. Take what influencers say with a grain of salt. Take what AI says, and use those as all launching pads to find better advice.”

That said, the TIAA Institute’s P-Fin Index shows U.S. adults correctly answer only 49% of personal finance questions, a figure unchanged since 2017. The gap is more pronounced among women.

The problem is not a lack of resources, but a lack of pipeline, Stanberry said. Take the Mercury study for example. Nearly half of the couples said they still learn money management by making mistakes.

The fix, she argues, is not to reduce financial literacy to spreadsheet fluency.

“We have a vision for how we want our lives to look — the things we want to do, the kind of home we want to live in, the kind of careers we want to have, the number of children — and those are all money decisions,” Stanberry said. “Financial literacy works by not crunching numbers, but being goal-based.”

Couples Fintech Comes In

The resource abundance of this moment, podcasts, apps, newsletters, courses, has not moved the literacy needle. What builders need to solve for is not more information. It is context-appropriate delivery at the right moment, Stanberry said.

“Meeting people where they are is essential,” she said. “And I’m not sure where we do that yet.”

Fintechs in the “finances for couples” space are trying to do just that in consumer products to give couples shared visibility into spending and goals while letting them retain individual control. Companies operating here are just a piece of the global personal finance software market valued at $1.35 billion in 2025, and that is projected to nearly double over the next decade.

For example, Monarch Money raised $75 million at an $850 million valuation in 2025, and is positioning itself as an operating system for personal finance. Tandem, a Chicago-based app for couples who want financial transparency without joint accounts, was acquired by Reseda Group in 2025. Meanwhile, Honeydue handles joint expense tracking for free.

On Mercury’s side, the historically startup banking company, launched its Mercury Personal product last year which allows for shared accounts and flexible access for more collaborative money management.

Stanberry adds a note of caution for any product in this space:

“You want to make sure that you still have a little bit of friction and that you’re still talking to your partner,” she said. “Don’t let the app just completely take over and allow you to avoid all the money conversations.”

The Confidence You Already Have

Conversations about money are important no matter if managing it at work or at home. Couples should be supporting shared leadership and not defaulting to primary and secondary users, Stanberry said.

Much of that work is already happening, but people don’t always see it as leadership. They aren’t good at putting into words what they are actually already doing, Stanberry said.

As such, she hopes Mercury repeats “The New Economics of Modern Love,” report in five years and that results will show an increase in women feeling more confidence about how they are managing their money.

“Women don’t give themselves credit for the many tasks and responsibilities they have at home, and how that might translate to the workplace,” Stanberry said. “And then also what we do at the workplace and how that might translate to the home.”