Banking on Trust in a Tightening Economy

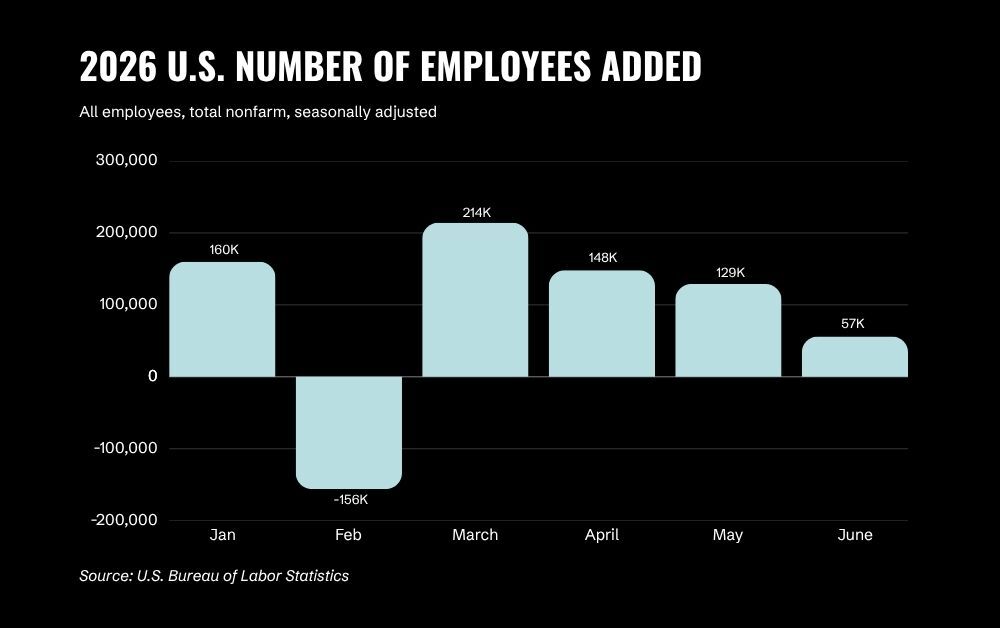

Last week, we dug into the impact of the changing labor market on fintechs’ strategy. This week bears a fresh report from the Bureau of Labor Statistics, and alas, the mixed signals continue. The U.S. added just 57,000 jobs last month, the weakest hiring month since February, though unemployment ticked down just a bit from 4.3% to 4.2%. Are employers hesitant to add headcount, or will we see a revival this month? We’re holding our breath to find out.

And as the economic landscape remains shaky, the stakes get higher in banking too. Businesses and consumers now, more than ever, are turning to tools that can help them identify unnecessary expenses and hedge for this uncertain future. To what extent can AI help navigate these questions on humans’ behalf? How exactly can firms build users’ trust in AI-powered tools that touch something as sensitive as their financial health?

Today, we unpack lessons from Mercury’s VP of Product, Ryan Wiggins, after a decade exploring the same trust challenges at Facebook and WhatsApp. But in banking, the margin for error is much smaller. In AI-powered banking, 12-month roadmaps are too slow, 90 days of financial data is no longer enough, and human permission matters way more than reducing friction.

-The Editors